In today’s globalized world, where electronics have become an integral part of our daily lives, concerns about the environmental impact of these devices have taken center stage. To address these concerns and pave the way for a more sustainable future, the European Union introduced the RoHS Directive. This directive represents a significant step towards reducing hazardous substances in electronic products and promoting eco-friendly manufacturing practices. In this article, we will explore the RoHS Directive, its purpose, and which companies need to adhere to its regulations.

Why was the RoHS Directive put into place?

The RoHS Directive, short for the Restriction of Hazardous Substances Directive, was put into place to address the growing concerns surrounding electronic waste and the environmental impact of hazardous substances found in electrical and electronic equipment (EEE). It was first adopted by the European Union in 2003 and later revised in 2011 (RoHS 2) and 2015 (RoHS 3).

The primary objectives of the RoHS Directive are as follows:

Environmental Protection: To reduce the environmental impact of EEE by restricting the use of hazardous substances in their production.

Public Health: To safeguard the health and safety of consumers and workers who come into contact with EEE.

Recycling and Waste Management: To facilitate the recycling and proper disposal of electronic waste, minimizing the release of hazardous substances into the environment.

What is the RoHS Directive?

The RoHS Directive sets strict restrictions on the use of specific hazardous substances in electrical and electronic equipment. These substances are:

Lead (Pb)

Mercury (Hg)

Cadmium (Cd)

Hexavalent chromium (Cr⁶⁺)

Polybrominated biphenyls (PBB)

Polybrominated diphenyl ethers (PBDE)

Under the directive, the maximum permissible concentration of these substances is set at 0.1% by weight in homogeneous materials for lead, mercury, hexavalent chromium, PBB, and PBDE, and 0.01% for cadmium.

It’s essential to note that RoHS applies to a wide range of electrical and electronic equipment, including household appliances, consumer electronics, lighting, medical devices, and industrial equipment. Manufacturers, importers, and distributors of these products must ensure that they comply with RoHS regulations before placing them on the European market.

Which companies need to work under the RoHS Directive?

The RoHS Directive applies to various types of businesses involved in the production and distribution of electrical and electronic equipment within the European Union. These companies include:

Manufacturers: Companies that produce EEE or components of EEE that contain the restricted substances must ensure their products comply with RoHS regulations.

Importers: Entities that import EEE into the EU market, whether as finished products or components, are responsible for verifying that the items meet RoHS requirements.

Distributors: Distributors within the EU are obligated to ensure that the EEE they supply complies with RoHS regulations. They should obtain compliance documentation from manufacturers or importers.

In conclusion, the RoHS Directive is a vital piece of legislation aimed at mitigating the environmental and health risks associated with hazardous substances in electrical and electronic equipment. By restricting the use of these substances and promoting eco-friendly manufacturing practices, the directive contributes to a greener and more sustainable future. Companies involved in the production, import, or distribution of EEE in the EU must diligently adhere to the RoHS regulations to ensure compliance and promote environmental responsibility.

The REACH regulation, having been in effect for several years now, has rapidly become a widely accepted and influential standard in the world of chemical regulation. Since its adoption in 2006 and its full implementation in 2018, REACH has consistently proven its effectiveness in enhancing the safety and sustainability of the chemical industry within the European Union (EU) and beyond.

Over the years, REACH has successfully streamlined and replaced various existing EU chemical regulations, creating a unified and comprehensive framework for the registration, evaluation, authorization, and restriction of chemicals. This harmonized approach has not only simplified compliance for companies but has also improved the transparency and accessibility of chemical information for both industry stakeholders and the public. Furthermore, the influence of REACH has extended beyond the borders of the EU. Many countries and regions have looked to REACH as a model for their own chemical regulations, recognizing its effectiveness in safeguarding public health and the environment. Initiatives similar to REACH have emerged in various parts of the world, solidifying REACH’s reputation as a global standard in chemical management.

This article sheds light on the REACH Regulation, delving into its origins, its scope, and the companies it impacts.

Why was the REACH Regulation put into place?

Environmental Protection: One of the primary motivations behind the establishment of the REACH Regulation was the need to protect the environment. Prior to REACH, the use of chemical substances was governed by a patchwork of regulations, often with inadequate oversight. This led to widespread pollution, contamination of water bodies, and adverse effects on ecosystems. REACH was designed to mitigate these environmental risks by promoting the responsible use of chemicals.

Human Health: Another critical concern addressed by REACH is the protection of human health. Many chemical substances can have detrimental effects on individuals who come into contact with them, whether through direct exposure or the consumption of contaminated products. REACH aims to ensure that chemical substances used in the EU do not pose undue risks to human health, particularly for workers in industries where these substances are commonly used.

Promoting Innovation: While the primary focus of REACH is safety, it also encourages innovation. By requiring manufacturers and importers to provide detailed information about the chemicals they produce or import, REACH enables safer product development and fosters the creation of alternative, less hazardous substances.

What is the REACH Regulation?

Registration: Under REACH, companies that manufacture or import chemical substances into the EU in quantities exceeding one ton per year are required to register them with the European Chemicals Agency (ECHA). This registration includes providing data on the substance’s properties, uses, and potential risks.

Evaluation: ECHA evaluates the data submitted by companies to assess the safety of chemical substances. If a substance is found to pose a risk to human health or the environment, ECHA can impose restrictions or recommend authorization for its use.

Authorization: Certain substances of very high concern (SVHC) may require specific authorization for use. Authorization is granted only if the use is deemed essential, and adequate control measures are in place to minimize risks.

Restriction: REACH empowers the EU to restrict the use of hazardous substances if they pose an unacceptable risk. Restrictions can encompass limitations on production, import, and use of such substances.

Communication: REACH emphasizes the importance of information sharing along the supply chain. Manufacturers, importers, and downstream users are obligated to communicate information on safe handling, risks, and risk mitigation measures.

Which companies need to work under the REACH Regulation?

Since 2006, companies that produce chemical substances within the EU or import them into the EU, regardless of their location, must adhere to REACH requirements. This includes not only chemical manufacturers but also producers of articles (products) containing substances that may be released during their use. Companies that import chemical substances into the EU from outside the EU/EEA must also comply with REACH. They share the responsibility for ensuring the safe use of these substances in the European market. Businesses that use chemical substances in their processes or products, such as industrial manufacturers, must follow the safety measures recommended in the Safety Data Sheets provided by suppliers and communicate relevant information to their employees.

In conclusion, the REACH Regulation stands as a robust framework dedicated to safeguarding both the environment and human health. By promoting the responsible use of chemical substances, it not only addresses past challenges but also contributes to a safer and more sustainable future. Companies within the EU and those wishing to engage with the European market must understand and adhere to REACH, ensuring that their activities align with its goals of protecting people and the planet.

“BMW is the place where I can have the biggest impact possible in my situation and a lot of powerful resources to enable change.”

What does sustainability mean for you?

Janine Thies: “For me, it is understanding the boundaries of our planet – full stop. That’s the most essential part of sustainability: understanding that there are limited resources and that it’s my responsibility to make sure I make a positive impact and contribute to conserving where we live. For me, it’s an elementary term.”

And in regards to this, what motivates you to work in sustainability?

JT: “It’s more of a passion than a job description. I’ve always felt very connected to nature since I was a kid. It was natural for me to be in nature for hours. I didn’t need any toys, but I needed to be out in nature and explore. Everything – every stone or leaf – has a meaning or a task. It’s fascinating that, in nature, everything makes sense.

Since we are also part of nature, I always seek to answer the question: What is my part in that system? This is what motivates me every day.”

How did you become a circular economy manager?

JT: “I can say I grew up with a sustainable mindset. My dad is an architect, and in our home, everything’s focused on natural materials. And to be honest, when I was a kid, I didn’t like that. But my dad made me understand that there are natural and artificial materials and their benefits and disadvantages.

I studied Russian, English, and business economics. After my studies, I started working at BMW as a so-called brand protection manager. I worked in the field of counterfeits where we were looking for fake manufacturing buildings where BMW parts got produced in an unauthorized way. These parts are not safe, and some customers can’t distinguish the original from the fake. I was responsible for the US and the Russian market. The peak of working as a brand protection manager was finding the manufacturing buildings where they produced the fake parts. In the US, I worked with the FBI a lot. When we located a building, they would raid the building while we would wait in a secured car nearby. You can really imagine it like you see it in movies.

Why do I tell you all of this? One day, one of the FBI agents I grew friends with was sitting next to me while a raid was happening and asked me: Why do you actually do that job? He asked me this because I would always talk to him about the urgency of changing our economy because of climate change. At that moment, I gave him the usual answer: Because we want the BMW customers to be safe from fake parts. But on my flight back to Germany, his question really had me thinking. I realized that the job of a brand protection manager was not what I was passionate about. So, all of a sudden, I decided to write a business case for the materials we found when we did our raids. Up to then, all materials found in raids were scraped. And this is how I found myself calculating how we could recycle and reuse the material while I was on the plane back to Germany.

Long story short: This is how I came to change jobs inside BMW and join their task force for a circular business. The task force, which I was a founding member of, grew very successful, and BMW created a venture out of it.

I didn’t join the joint venture but decided to join the recycling and dismantling team of BMW and became a circular economy manager.”

What are some things that you do to make your own life more sustainable?

JT: “Six years ago, I decided not to fly anymore. It just didn’t feel right to fly to a conference and then talk about the importance of sustainability on stage. That’s one thing.

Another thing is that I rarely eat meat, and if I do, it is from the region I live and very sustainably farmed. The third thing, of course, is talking with my kids about being part of nature and giving back so they grow up with the mindset of being part of nature.

And the fourth thing is supporting my husband’s business to grow more sustainable. He’s been a leadership trainer for 19 years, and four years ago, he changed his training into being in nature. To see how it developed and a lot of high-level management come there and understand the importance of being in balance with nature is really cool.”

What is something new you learned in the past year?

JT: “I learned something about myself. Big companies like BMW oftentimes get a lot of hatred, claiming that they could and should do a lot more for sustainability than they already do. What they forget is how eager and passionate sustainability people work at these kinds of global players. However, this totally affects me. I´m continuously questioning myself if I was in the right place. I´m absolutely impact-driven and realized that the needed shift in our economy needs all global players driven by passionate employees.

So, for me, BMW is the place where I can have the biggest impact possible in my situation and a lot of powerful resources to enable change.”

What do you think companies lack to become better at sustainability?

JT: “While a lot of people talk about technology, I’d say even more than technology, we need better people. As a keynote speaker, I get some deep insights into companies, and what most companies lack is investing in the development of their employees. These companies need to understand that sustainability is also a personal decision. People need to ask themselves what kind of world they want to create for their families and friends and how they can match their motivation with their daily work. Sustainability needs more than what is said in most job descriptions. If companies decide to come up only with technological solutions and they don’t develop the people and mindsets behind it, it’s not gonna work out.”

What would you rate your most successful measure for more sustainability and or circularity in the last years and why?

JT: “Eight years ago, I would have said it’s creating that business case. Next would be the founding of the joint venture. Today, looking back at the last 14 years, I’d say it is understanding how to create momentum for the people I talk to – no matter if it is in a one-on-one conversation or if I’m standing in front of hundreds of people on stage. I found a way to – in a matter of 30 minutes – take people on the personal journey of finding what is important to them, how to match that to their work, and creating concrete measures from it that they can apply straight away. And the best part: The measures are not only sustainable, they’re also profitable. I’d call that my biggest achievement of the last two years, especially because the thoughts I provoke are often multiplied by the people I talk to.”

What would you wish for from a legislative point of view?

JT: “Overall, I think sustainable decisions should be made easier for consumers from a monetary point of view. I don’t understand why, in Germany, we need to pay more taxes on vegetarian food than on non-vegetarian food. Why is flying as cheap as it is worldwide, or even owning a private jet?

Why are big oil companies allowed to destroy nature/ people, although they have been knowing their effects on climate change and human health for decades?

I think everyone can be part of the solution if laws, subventions, and tax reliefs focus on the real big levers and support the needed shift towards an economy that´s in peace with Mother Nature.”

With the growing importance of batteries in the green transition, the EU aims to create a circular economy for the battery sector, addressing every stage of a battery’s lifecycle. This initiative is particularly crucial, given the anticipated ten-fold increase in battery demand by 2030. By replacing the 2006 batteries directive and enhancing waste management legislation, the regulation sets a new standard for sustainability, safety, and end-of-life management of batteries on a global scale.

What is the EU Battery Regulation?

The European Battery Regulation, passed by the European Parliament and the Council in August 2023, applies to all economic operators involved in the EU battery market. This includes manufacturers, producers, importers, and distributors, covering a broad range of batteries. The regulation encompasses waste portable batteries, electric vehicle (EV) batteries, industrial batteries, starting, lighting, and ignition (SLI) batteries, and batteries for light means of transport (LMT), such as electric bikes, e-mopeds, and e-scooters.

Under these regulations, EV batteries, LMT batteries, and rechargeable industrial batteries exceeding two kWh must carry a “clearly legible and indelible” carbon footprint declaration and label, detailing key information like recycled cobalt, lead, lithium, and nickel content. Economic operators must also adopt and communicate due diligence policies for critical raw materials supply, following international standards such as the OECD Due Diligence Guidelines and the UN Guiding Principles on Business and Human Rights.

Additionally, the introduction of a digital battery passport for certain batteries enhances traceability, providing data on the battery model, specific usage, and more. All batteries, regardless of type, must carry labels and QR codes indicating capacity, performance, durability, chemical composition, and the “separate collection” symbol. Notably, the “CE” mark is now required for all batteries to demonstrate conformity with EU health, safety, and environmental standards, with labeling affixed directly on the device rather than the battery itself.

The regulation’s core objective is to foster a circular economy in the battery industry by imposing comprehensive requirements throughout the battery lifecycle. This includes collection targets, material recovery goals, and extended producer responsibility.

Producers are mandated to meet collection targets for waste portable batteries (63% by 2027, 73% by 2030) and have a dedicated collection objective for waste LMT batteries (51% by 2028, 61% by 2031). Moreover, the regulation sets ambitious targets for lithium recovery from waste batteries (50% by 2027, 80% by 2031), with potential adjustments based on market and technological developments.

Minimum recycled content levels are established for industrial, SLI, and EV batteries (initially 16% for cobalt, 85% for lead, 6% for lithium, and 6% for nickel), supported by mandatory recycled content documentation. Recycling efficiency targets are set at 80% for nickel-cadmium batteries by 2025 and 50% for other waste batteries by 2025.

The regulation also ensures that, by 2027, portable batteries incorporated into appliances should be removable and replaceable by end-users, benefiting consumers. LMT batteries must be replaceable by independent professionals.

The European Battery Regulation is scheduled to take effect on 17 August 2023, with enforcement commencing from 18 February 2024. It features a phased approach to rule implementation:

August 2024:

Economic operators, aside from due diligence policies and end-of-life management, will begin complying with their obligations.

Conformity assessment procedures for batteries, with exceptions, start applying.

August 2025:

Rules pertaining to end-of-life battery management must be adhered to.

Penalties for violations are to be established by Member States, aiming for effectiveness, proportionality, and deterrence.

January 2026: Labeling and information requirements will be applicable, with QR code implementation deferred until 2027.

February 2027: Companies must ensure removability and replaceability of portable and LMT batteries.

By 31 December 2030, the Commission will assess the feasibility of extending carbon footprint declaration requirements to portable batteries and implementing a maximum life cycle carbon footprint threshold for rechargeable industrial batteries with a capacity of two kWh or less.

How to prepare for the EU Battery Regulation

To prepare for compliance with the European Battery Regulation, companies in the battery industry should take several key steps.

Firstly, it’s essential to thoroughly understand the regulation’s specific requirements and deadlines. This means investing time in comprehending the nuances of the regulation as it relates to your particular role and scope within the battery market.

Simultaneously, a comprehensive assessment of current operations is necessary. This involves a detailed evaluation of existing battery products, manufacturing processes, and supply chains. The aim is to identify areas that require adjustments and modifications to align with the regulation’s rigorous standards.

In parallel, companies must establish due diligence policies for the sourcing of critical raw materials, including cobalt, graphite, lithium, nickel, and others. These policies should conform to internationally recognized standards such as the OECD Due Diligence Guidelines and the UN Guiding Principles on Business and Human Rights. Ensuring transparency and responsibility within the supply chain is not only a regulatory requirement but also integral to sustainable business practices.

By proactively addressing these aspects, companies can position themselves for successful compliance with the European Battery Regulation. This not only ensures adherence to regulatory obligations but also aligns with broader sustainability objectives, contributing to a more environmentally responsible and circular battery industry in line with the EU’s green transition objectives.

In a bid to combat carbon emissions and level the playing field for European businesses, the European Union (EU) has introduced the Carbon Border Adjustment Mechanism (CBAM). This mechanism, part of the EU’s “Fit for 55” package, aims to put a price on greenhouse gas emissions associated with imports compared to products produced within the EU. It also ensures that domestic manufacturers have equal competitive opportunities concerning greenhouse gas costs compared to their counterparts in non-EU countries.

Why was CBAM implemented?

The EU’s goal is ambitious: to reduce carbon dioxide (CO2) emissions by 55% by 2030 compared to 1990 levels. As part of this initiative, the EU has been gradually reducing the free allocation of EU Emissions Trading System (EU-ETS) certificates to energy-intensive industries. This reduction creates a risk of companies in certain sectors shifting their production to Non-EU countries due to cost considerations, potentially undermining the effectiveness of the EU’s emissions reduction measures.

While EU-based businesses are already required to account for the carbon footprint of their production, CBAM extends this requirement to businesses importing goods from outside the EU, making importers of CBAM-covered products pay a carbon price to mitigate potential competitive disadvantages for domestic manufacturers of similar goods.

What is CBAM?

CBAM necessitates a carbon price on the import of specific goods produced outside the EU based on their associated carbon emissions. The price per CBAM certificate is determined by the average weekly price of EU Emissions Trading System (EU-ETS) certificates and multiplied by the number of CBAM certificates to be surrendered. Each CBAM certificate corresponds to one tonne of emitted CO2 (carbon dioxide), N2O (nitrous oxide), or F-gases (perfluorinated hydrocarbons) released during the production process of the imported goods.

Importers can claim a reduction in the number of CBAM certificates to be surrendered if they can demonstrate that a carbon price was paid in the country of origin.

Which companies are affected by CBAM?

The following product categories are set to be included in CBAM starting from October 2023:

Fertilizers (including precursor products such as ammonia and potassium nitrate)

Cement (including bricks, clay cement, and other kaolin-containing clay and earthware)

Iron (agglomerated iron ores and concentrates) and steel (including downstream products)

Aluminum (including downstream products)

Electrical energy

Hydrogen

Important: CBAM applies for companies that import the above materials but also for companies that import processed goods containing the above materials (especially for aluminum and steel)

In the coming years, there are plans to expand the scope of CBAM to include all goods covered by the EU Emissions Trading System (ETS). Non-EU countries integrated into the EU Emissions Trading System or whose emissions trading systems are recognized as equivalent may be exempted from CBAM.

CBAM Status and Timeline

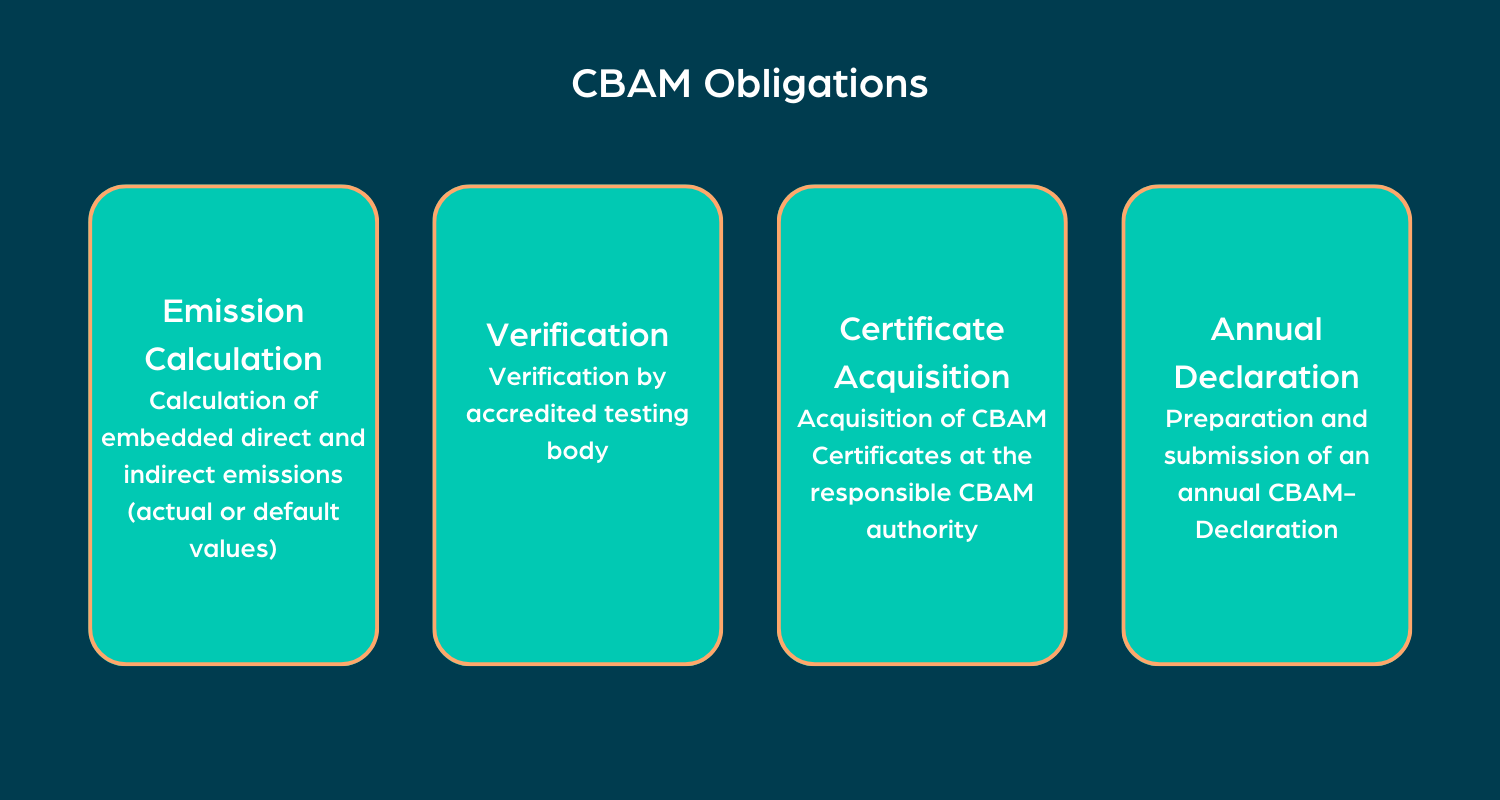

CBAM will be introduced gradually, beginning with a transitional phase from October 1, 2023, to December 31, 2025. During this period, companies will be required to calculate and document the direct and indirect emissions associated with the production process of imported goods subject to CBAM. They must submit quarterly reports, known as CBAM reports, by January 31, 2024, providing data on the quantity of imports, direct and indirect CO2 emissions abroad, and the potential carbon price paid in the country of origin. The CBAM report is submitted using the CBAM Transitional Registry which will be deployed for the use of Economic Operators in the EU as from the 1st of October 2023 together with a set of webinars and trainings which will facilitate the use of the registry and the submission of data during the transitional period. However, no financial compensation through the surrender of CBAM certificates is required during this phase.

From January 1, 2026, CBAM will fully come into effect. At this point, companies will face more extensive obligations, including the need for a CBAM registration for the status of an “Authorized Declarant.” They must calculate the embedded direct and indirect emissions of imported goods into the EU, have the reported data on direct and indirect emissions verified by an accredited testing body, purchase the required number of CBAM certificates through a central platform to cover the embedded direct and indirect emissions, and submit an annual CBAM declaration by May 31 of each calendar year for emissions associated with goods imported in the previous year.

How to prepare for CBAM

Preparing for the implementation of the Carbon Border Adjustment Mechanism (CBAM) requires proactive measures. Companies should begin by conducting a comprehensive assessment of their supply chains to identify products that fall under CBAM’s purview. This involves calculating the direct and indirect emissions associated with their imported goods and considering potential carbon pricing mechanisms in the countries of origin. To streamline compliance, businesses should invest in robust data collection and reporting systems. Additionally, they should monitor updates and guidelines provided by regulatory authorities to ensure alignment with CBAM requirements. Ultimately, preparation for CBAM hinges on a combination of thorough assessment, technological readiness, and collaboration between public and private sectors to navigate the transition successfully.

The European Union (EU) stands out as a global leader in enacting highly sophisticated, stringent, forward-thinking, and intricate corporate and investor sustainability laws, along with comprehensive reporting requirements within its economic domain. Embracing the overarching ‘European Green New Deal’, Europe is actively executing an extensive array of measures aimed at combatting climate change, fostering sustainable innovation, and achieving climate neutrality across the continent by 2050. In this guide, we will delve into the European Green Deal, examining its core elements and the reporting regulations it entails, while assessing whether the regulations and directives represent solely an additional task or a unique opportunity.

The European Green Deal

The European Green Deal is a comprehensive and ambitious policy framework introduced by the European Commission, the executive branch of the European Union, in December 2019. It serves as a roadmap and action plan to transform the EU into a sustainable, climate-neutral, and environmentally friendly economy by 2050. The deal aims to tackle climate change, biodiversity loss, and environmental degradation while promoting a just and inclusive transition.

Why was the European Green Deal put into place?

The roots of the European Green Deal can be attributed to several key factors. Firstly, the adoption of the Paris Agreement in 2015 laid the foundation for international efforts to limit global warming to below 2 degrees Celsius, with an ambitious target of 1.5 degrees Celsius. As a party to the agreement, the EU made commitments to take bold measures in reducing greenhouse gas emissions.

Additionally, there has been a noticeable shift in politics, with EU member states, policymakers, and citizens recognizing the urgency of addressing climate change and embracing environmental protection and sustainability as fundamental priorities for the region.

Moreover, the rise of environmental movements and increased public awareness and activism has exerted significant pressure on political leaders, compelling them to take more decisive actions towards achieving sustainability goals. These factors combined have paved the way for the formulation and implementation of the European Green Deal, signaling the EU’s commitment to leading the fight against climate change and promoting a greener and more sustainable future.

How does the European Green Deal work?

The European Green Deal acts as a guiding roadmap and action plan, directing the EU’s policies and initiatives for the foreseeable future. Its implementation involves a multifaceted approach, comprising legislative measures, funding mechanisms, and collaborative efforts with member states, businesses, civil society, and international partners.

Under the umbrella of legislation and regulation, the European Commission formulates and enacts new laws and regulations to support the Green Deal’s objectives. This entails establishing targets, standards, and guidelines aimed at promoting sustainable practices across various sectors.

To facilitate the realization of its goals, the EU provides substantial funding through diverse mechanisms such as the Just Transition Fund, the European Green Deal Investment Plan, and the EU’s long-term budget (Multiannual Financial Framework).

The success of the Green Deal hinges on fostering cooperation and partnerships with EU member states, businesses, local authorities, and civil society organizations. This collaborative approach is crucial for effective implementation and continuous monitoring of the initiatives.

Regular monitoring and reporting by the EU play a vital role in evaluating the progress made towards achieving the Green Deal’s objectives. This fosters transparency, ensures accountability, and allows for necessary policy adjustments and actions as circumstances evolve.

The European Green Deal Objectives

The European Green Deal represents a collective effort by the EU to address the pressing challenges posed by climate change and environmental degradation while fostering economic growth and social well-being within a sustainable framework. It involves legislation, funding mechanisms, and collaborations between member states, industries, and civil society to achieve its ambitious goals. Key objectives of the European Green Deal include:

Climate Neutrality: The primary goal is to make Europe the world’s first climate-neutral continent by 2050. This entails reducing greenhouse gas emissions to net-zero levels, where any remaining emissions are offset by measures such as carbon capture or reforestation.

Clean Energy: The deal emphasizes the adoption of renewable and clean energy sources, reducing reliance on fossil fuels, and promoting energy efficiency to achieve a sustainable energy system.

Circular Economy: The EU aims to transition towards a circular economy that minimizes waste, promotes recycling, and encourages the sustainable use of resources.

Biodiversity and Ecosystems: The Green Deal aims to protect and restore biodiversity, enhance ecosystem resilience, and combat pollution to ensure the long-term health of the environment.

Sustainable Agriculture and Food Systems: The deal seeks to promote sustainable agricultural practices, reduce the environmental impact of food production, and support more sustainable food consumption patterns.

Sustainable Mobility: The EU aims to promote clean and sustainable transport options, including increased use of electric vehicles, improved public transportation, and cycling infrastructure.

Renovation of Buildings: The Green Deal emphasizes improving the energy efficiency of buildings to reduce emissions and enhance the overall sustainability of the construction sector.

Just Transition: The deal emphasizes the importance of a fair and inclusive transition, ensuring that the changes in economic and industrial practices do not disproportionately affect vulnerable communities and workers.

An Overview: European Sustainability Reporting Regulations

The European Green Deal entails various reporting regulations aimed at monitoring and assessing progress towards its sustainability goals. These reporting regulations aim to enhance transparency, accountability, and informed decision-making in pursuit of the European Green Deal’s ambitious sustainability goals. By requiring organizations to disclose their environmental and climate-related data, the EU seeks to drive positive change and ensure a collective effort towards building a climate-neutral and environmentally responsible continent.

Circular Economy and Waste Management:

The EU has been actively promoting a circular economy model, which aims to minimize waste, extend product lifetimes, and enhance resource efficiency. This section explores EU directives and regulations concerning waste management, recycling, and eco-design, as well as the promotion of sustainable production and consumption patterns.

Ecodesign for Sustainable Products Regulation (ESPR)

What is it?

The ESPR aims to expand the Ecodesign directive’s scope to cover a wide range of goods beyond energy-related products. It sets criteria for most physical items in the EU market, excluding some like food. It enhances eco-friendliness and energy efficiency through tailored ecodesign requirements. Notably, it introduces the Digital Product Passport (DPP) for better product information.

Who needs to comply?

All companies introducing products to the EU market, regardless of origin, must comply with the ESPR. This includes a wide range of products, even extending to military, space, and medical items. The ESPR framework covers various entities in the value chain, such as manufacturers, importers, distributors, retailers, and sellers.

When does it come into action?

The current Ecodesign Directive is active until the transition to the ESPR. The ESPR will replace the current directive upon implementation. The 2022-2024 work plan includes acts for mobile phones, tablets, computers, and servers. 31 product categories will be assessed, focusing on energy and material efficiency, potentially leading to regulations by 2030. The phase emphasizes criteria like durability, reparability, and recyclability. Deadlines and transitions will be detailed in post-ESPR adoption delegated acts, as implementation is expected from 2024 to 2030.

The Digital Product Passport (DPP) is a concept introduced under the Ecodesign for Sustainable Products Regulation (ESPR). It aims to provide comprehensive and standardized information about a product’s environmental and sustainability attributes throughout its entire lifecycle. The DPP is a digital document or database that accompanies a product from its design and manufacturing stages to its use, maintenance, and eventual disposal or recycling.

Key features of the Digital Product Passport:

Product Information: materials, components, energy efficiency, environmental impact, repairability, etc.

Lifecycle Data

Repair and Maintenance: guidelines for repairing and maintaining the product, extending its lifespan and reducing the need for premature disposal

Recycling and Disposal: how the product can be disassembled, recycled, or disposed of properly

Traceability and Transparency: a traceable record of the product’s origin, manufacturing processes, and environmental impact

The introduction of the Digital Product Passport is aimed at fostering a more sustainable approach to product design, manufacturing, and consumption. It empowers consumers to make environmentally conscious choices, encourages manufacturers to produce longer-lasting and more eco-friendly products, and contributes to the overall transition towards a circular economy.

Sustainable Finance and Investment:

The EU is working on aligning financial systems with sustainability objectives. This section covers the EU Taxonomy for sustainable activities, the Sustainable Finance Disclosure Regulation, and other measures to encourage green investments and responsible financial practices.

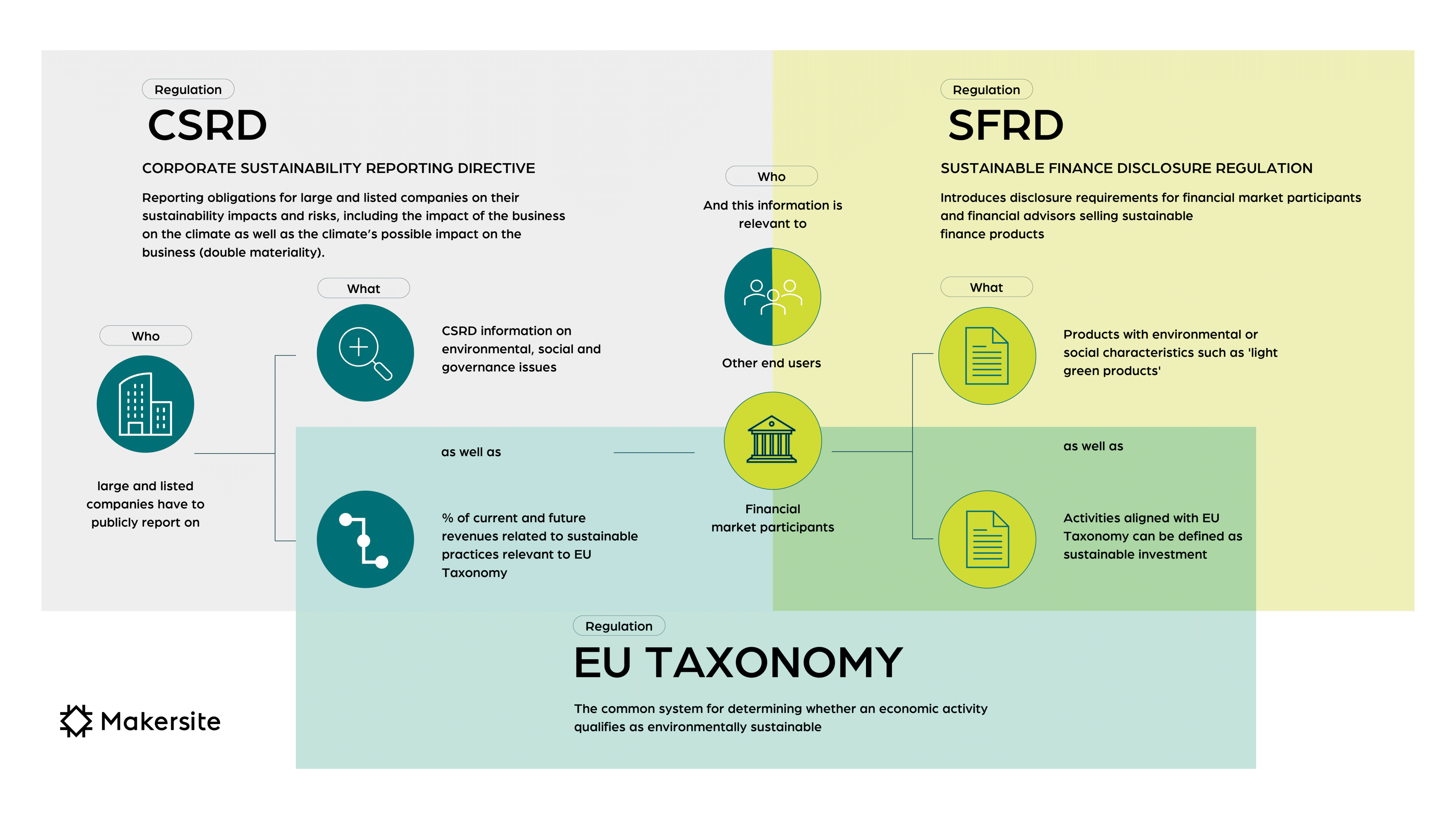

Sustainable Finance Disclosure Regulation (SFDR)

What is it?

The Sustainable Finance Disclosure Regulation (SFDR) is a financial reporting framework that promotes transparency regarding sustainability. It mandates financial market participants and advisors to reveal how they address sustainability risks and impacts in their products. Suppliers of investment products must disclose how they communicate sustainability considerations to clients. SFDR aims to enhance transparency in the sustainability of financial offerings and prevent misleading claims of sustainability (greenwashing) often associated with investment funds.

Who needs to comply?

SFDR compliance is necessary for financial market participants (FMPs) and financial advisors. Any company involved in creating and offering financial products must adhere to SFDR, alongside existing disclosure requirements.

When does it come into action?

The SFDR has been in place since 2019 and the concerned parties need to report against it since 2021.

EU taxonomy

What is it?

The EU Taxonomy is a guide that categorizes economic activities as environmentally sustainable or not. Starting in 2023, companies and investors must report how well their actions align with it. This helps measure their level of environmental friendliness. The Taxonomy focuses on six goals, including climate action, water protection, and circular economy. Financial institutions will report on the first two goals from January 1, 2023, with the remaining four added a year later.

The reporting obligation extends to all financial market participants, large companies, and SMEs listed on the stock exchange. If a company is based in Europe or operates a European legal entity with more than 500 employees, reporting is mandated.

When does it come into action? The EU Taxonomy will be implemented in stages. Starting from January 1, 2023, financial institutions will need to report the portion of their portfolio aligned with the EU Taxonomy. Initially, they will report on two environmental objectives related to climate change. The other four objectives will be added a year later. This reporting requirement applies to EU-registered companies for now.

Task Force on Climate-related Financial Disclosures (TCFD)

The Task Force on Climate-related Financial Disclosures (TCFD) is a reporting standard designed to encourage organizations to disclose information about their climate-related financial risks and opportunities. It was established by the Financial Stability Board (FSB) in 2015 and provides a framework for companies to voluntarily disclose information related to their governance, strategy, risk management, and metrics in relation to climate change. The TCFD framework aims to enhance transparency, enable better assessment of climate-related risks, and help investors, lenders, and other stakeholders make more informed decisions regarding the financial implications of climate change on businesses.

Corporate Social Responsibility and Reporting:

The EU has taken steps to encourage corporate social responsibility and sustainability reporting by businesses. This part discusses the Corporate Sustainability Reporting Directive (CSRD) and other initiatives that promote transparency and accountability in corporate sustainability practices.

The Corporate Sustainability Reporting Directive (CSRD)

What is it?

The CSRD, or Corporate Sustainability Reporting Directive, builds upon the NFRD by expanding reporting requirements for companies on ESG matters like environmental impact, social policies, and human rights. It introduces new aspects such as reporting future-oriented sustainability goals, adverse effects, and intangible resources. The CSRD also introduces “double materiality,” compelling companies to consider both their impact on the environment and potential environmental impacts on their future, while mandating independent verification, integration of sustainability reporting into management reports, and the use of machine-readable formats for transparency. The European Financial Reporting Advisory Group (EFRAG) is developing reporting standards to ensure consistency and transparency.

Who needs to comply?

The CSRD requires compliance from NFRD-reporting companies and includes new criteria: firms with 250+ employees, €40M+ net sales, or €20M+ balance sheet, plus most listed companies (except small ones) and non-EU companies with €150M+ EU sales for two years.

When does it come into action?

The NFRD rules are effective until CSRD implementation. Starting January 2024, large public interest companies (500+ employees) must follow CSRD. From January 2025, other eligible companies must comply. By January 2026, stock-exchange-listed SMEs (without postponement) also need to adhere to CSRD.

However, in October 2023 the European Commission announced plans to delay key aspects of CSRD, specifically the adoption of requirements for companies to provide sector-specific sustainability disclosures and for sustainability reporting from companies outside of the EU.

Announced alongside the Commission’s release of its 2024 Commission Work Programme – designed to set out a list of actions it will take over the upcoming year – the statement outlines the EU Commission’s intention to postpone the adoption date for the sector-specific European Sustainability Reporting Standards (ESRS) by two years. Additionally, it recommended delaying the adoption of rules for large non-EU companies that operate in the EU to provide sustainability reporting by 2 years.

As the Commission notes in its proposal, the postponement of these two key rules has arisen in order to allow “companies to focus on the implementation of the first set of ESRS,” “ensure that EFRAG has time to develop sectoral ESRS that are efficient,” and “limit the reporting requirements to the minimum necessary.”

Corporate Sustainability Due Diligence Directive (CSDDD)

What is it?

Note: Further CSDDD developments – where the directive failed to receive final approval – were announced on 28th February 2024. You can read about what happened here.

The CSDDD is an EU directive inspired by French and German laws, aiming to make companies address environmental and human rights risks in supply chains. It mandates risk assessment and mitigation, requiring large firms to align strategies with a sustainable economy and 1.5°C global warming limit. Proposed penalties of up to 5% of global sales are included for violations.

Who needs to comply?

The proposed directive lowers the threshold for companies affected, now including those with 250+ employees and over 40 million euros global turnover (compared to the earlier draft’s 500 employees and 150 million euros). Transition periods of up to five years are proposed to accommodate varying company sizes.

When does it come into action?

In 2023, the CSDDD has advanced significantly, with MEPs voting to enhance the original proposal. It’s currently in trilogue stage for negotiation among the European Parliament, Commission, and Council. A decision is expected soon, leading to implementation and mandatory company compliance with the directive’s provisions.

The Green Claims Directive enhances consumer protection rules, applying to both B2C and B2B marketing for explicit environmental claims. It mandates substantiation with scientific evidence, comprehensive life-cycle assessment, transparency in offsets, and a holistic approach to evaluating environmental impact. The directive complements existing regulations and emphasizes robust verification of environmental claims.

Who needs to comply?

The Green Claims Directive will impact most EU companies, including SMEs and large corporations in diverse sectors, and also non-EU companies targeting EU consumers. However, very small micro-SMEs (under ten employees or less than €2 million annual turnover) will be exempt from the requirements.

When does it come into action?

The European Commission introduced the Green Claims Directive on March 22, 2023. After its enactment, Member States will have 18 months to adopt it into their national laws. While implementation is anticipated by 2026, the timeline could shift based on EU negotiations.

European Sustainability Reporting Standards (ESRS)

In order to guarantee uniformity and openness in reporting, the European Financial Reporting Advisory Group (EFRAG) is in the process of formulating reporting standards for the CSRD, the so called European Sustainability Reporting Standards. The initial segment of these standards was projected to be released by November 2023, with the subsequent segment scheduled for publication in June 2024, but an October 2023 announcement by the EU Commission (see ‘The Corporate Sustainability Reporting Directive’, above) outlined their intention to postpone the adoption date for ESRS by 2 years.

Excerpt: Why Global Companies need to care about European Regulation

Global companies need to care about European sustainability reporting regulations because it directly impacts their access to European markets and smooth operations within the EU. Many global companies conduct business in the European Union or trade with EU member states. Compliance with European sustainability reporting regulations is essential to access these markets and ensure smooth operations without facing potential trade barriers or legal penalties. Moreover, adhering to these regulations provides a competitive advantage in a market where sustainability is increasingly valued.

The global trend towards sustainability reporting indicates that similar regulations may emerge in other regions, making compliance with European standards a strategic move for long-term viability and adaptability. For companies with complex supply chains extending to the EU, aligning with these regulations is essential to ensure seamless operations and avoid disruptions.

Sustainability Reporting: Struggle or Chance?

Sustainability reporting stands as a crucial tool in our modern world, aiming to bring transparency and accountability to the environmental, social, and governance (ESG) aspects of organizations. Yet, this endeavor does not come without its challenges, as it navigates the ever-shifting landscape of business, regulation, and public perception.

One of the primary struggles that sustainability reporting faces is the tension between its intent and the potential for “greenwashing.” Greenwashing occurs when companies present themselves as more sustainable than they truly are, often by manipulating data or focusing on a few positive aspects while downplaying their negative impacts. This dilutes the credibility of sustainability reports and erodes the trust of stakeholders who are seeking genuine efforts toward a more sustainable future.

Furthermore, the lack of standardized frameworks and guidelines for sustainability reporting poses a significant hurdle. With various reporting standards, such as GRI, SASB, and integrated reporting, organizations must choose which approach to follow. This diversity not only makes it challenging to compare different companies’ performance but also creates confusion among stakeholders about the true environmental and social implications of a company’s operations.

Financial constraints also hinder the comprehensive adoption of sustainability reporting. Small and medium-sized enterprises (SMEs) often struggle to allocate resources for data collection, analysis, and reporting on sustainability efforts. The upfront costs of setting up robust tracking systems and hiring specialized personnel can be daunting, making it difficult for smaller players to participate fully in this movement.

Legal and regulatory inconsistencies across different jurisdictions further complicate the sustainability reporting landscape. With varying requirements and expectations, multinational companies must navigate a complex maze of rules, sometimes leading to discrepancies in how they report their sustainability progress. This can create skepticism about the accuracy and reliability of the information presented in these reports.

To overcome these challenges, collaboration is key. Governments, regulatory bodies, businesses, and civil society must work together to establish clear and consistent reporting standards that are applicable globally. Moreover, technological advancements can play a crucial role in streamlining data collection and analysis, reducing the resource burden on organizations, especially SMEs.

However, despite these challenges, the importance of sustainability reporting cannot be underestimated. As stakeholders, including investors, consumers, employees, and regulators, demand greater transparency and responsible business practices, the pressure on organizations to improve their ESG performance intensifies. Companies that embrace sustainability reporting genuinely and integrate it into their core strategies can gain a competitive advantage by building trust and goodwill with stakeholders.

Summary

The EU’s sustainability regulations are comprehensive and wide-ranging, covering numerous sectors and aspects of modern life. By examining and adhering to these guidelines, businesses, governments, and individuals can actively contribute to a greener and more sustainable future for Europe and the planet at large. As the world faces increasing environmental challenges, the EU’s approach to sustainability regulation sets a precedent for other regions to follow and collectively work towards a more sustainable and resilient future.

The EU Taxonomy has emerged as a vital framework in the realm of sustainable finance and environmental accountability. With a focus on driving investments towards environmentally sustainable activities, the EU Taxonomy has implications for companies, investors, and the financial industry as a whole.

Why was EU Taxonomy put into place?

To fulfill the ambitious climate and energy targets set by the EU for 2030 and to align with the principles of the European Green Deal, a strategic shift towards funding sustainable initiatives is imperative. A crucial step in this journey involves channeling investments that promote environmental responsibility. However, to effectively navigate this transition, it is essential to establish a shared understanding and precise criteria for what qualifies as ‘sustainable’. Recognizing this necessity, the action plan on financing sustainable growth advocated for the establishment of a unified framework termed the “EU taxonomy”. By adopting a standardized approach, the EU aims to harmonize efforts, facilitate informed decision-making, and accelerate progress towards a greener and more resilient future.

What is EU Taxonomy?

The EU Taxonomy is a common classification system for sustainable economic activities. It sets out criteria for determining which activities contribute to six environmental objectives (see below). The taxonomy framework covers a wide range of sectors, such as energy, agriculture, manufacturing, and more.

All relevant companies are required to reveal how they integrate sustainability according to the taxonomy regulation. This involves disclosing EU taxonomy-aligned turnover, capital expenditure, and operating expenses. These disclosures should be included in non-financial reports, likely within the annual report or a dedicated sustainability report like the CSRD.

Environmental Objectives:

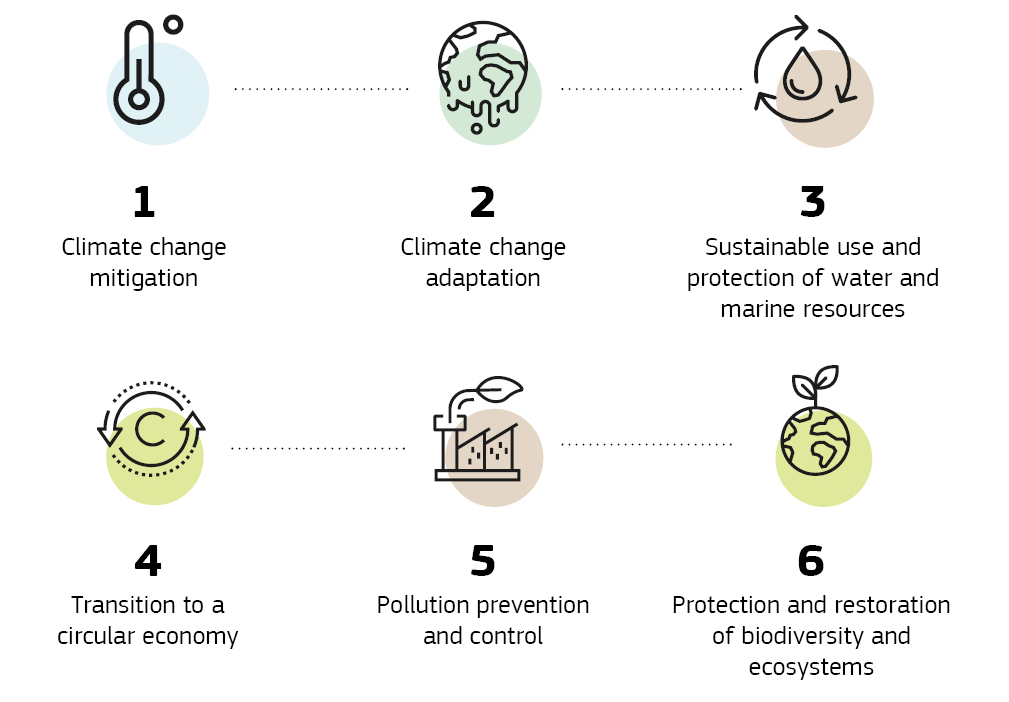

At the heart of the EU Taxonomy are six pivotal environmental objectives that collectively address the most pressing challenges humanity faces in terms of environmental degradation:

Climate Change Mitigation: Activities that contribute to reducing greenhouse gas emissions, such as renewable energy generation, energy-efficient technologies, and sustainable transportation, fall under this category.

Climate Change Adaptation: This objective encompasses activities that enhance society’s resilience to the impacts of climate change, including flood protection infrastructure, drought-resistant agriculture, and resilient urban planning.

Sustainable Use and Protection of Water and Marine Resources: Economic activities that promote the responsible management of water resources, prevention of water pollution, and conservation of marine ecosystems are covered here.

Transition to a Circular Economy: Activities related to recycling, reusing, and minimizing waste, as well as the design and production of products with extended lifecycles, fall within this objective, promoting a more sustainable consumption and production cycle.

Pollution Prevention and Control: This objective emphasizes activities that aim to prevent, reduce, and eliminate pollution, encompassing sectors such as clean technologies, waste management, and sustainable agriculture practices.

Protection and Restoration of Biodiversity and Ecosystems: Activities that contribute to conserving and restoring ecosystems, protecting biodiversity, and ensuring sustainable land use are included in this objective.

The Taxonomy Regulation establishes four key requirements for an economic activity to be deemed environmentally sustainable:

Significantly contributing to at least one environmental goal

Avoiding negative impact on the other five environmental goals

Adhering to basic safeguards

Meeting the specified technical screening criteria detailed in the Taxonomy delegated acts

Which companies must comply with EU Taxonomy?

EU taxonomy applies to large companies subject to the CSRD (NFRD), financial market participants (even those outside the EU) offering financial products in the EU, and the EU along with its member states when establishing green financial product standards. These entities are obligated to disclose how their investments align with the taxonomy’s criteria, facilitating transparency in sustainable finance practices.

EU Taxonomy Status and Timeline:

The EU Taxonomy was officially adopted in June 2020. It entered into force progressively, with its most impactful provisions taking effect from January 1, 2022. This marked the beginning of the disclosure requirements for larger companies and financial market participants. By January 1, 2023, additional disclosure obligations came into play. Over the coming years, more sectors and activities will be included, with the aim of making the EU Taxonomy an all-encompassing standard.

How to Prepare for EU Taxonomy:

Understanding the Criteria: Companies and financial market participants must familiarize themselves with the detailed technical screening criteria outlined in the taxonomy. This involves comprehending the metrics and thresholds set for each environmental objective.

Assessment and Reporting: Businesses need to assess their activities and investments against the taxonomy’s criteria. This process involves evaluating the degree to which their operations contribute to the specified environmental objectives. Clear and accurate reporting is essential to demonstrate alignment.

Engagement with Advisors: Collaborating with sustainability experts, consultants, and legal advisors can help ensure compliance and facilitate the integration of sustainability considerations into business strategies.

Investment Decisions: Financial market participants must integrate the taxonomy’s criteria into their investment decisions, ensuring that the investments they offer or manage are in line with it.

Conclusion

The EU Taxonomy stands as a landmark effort by the European Union to foster sustainable finance and promote environmentally responsible practices across industries. By providing a standardized framework for categorizing environmentally sustainable activities, the EU Taxonomy empowers investors and stakeholders to channel resources towards activities that contribute to a greener future. As its implementation continues to unfold, companies and financial market participants must remain vigilant in adapting their practices to align with it. Through collective efforts, the EU Taxonomy has the potential to drive lasting positive change and contribute to the global sustainability agenda.

“Instead of resisting change or clinging to outdated models, embracing uncertainty and cultivating a mindset of continuous learning is paramount. This lesson has reinforced the importance of flexibility, not just in strategies or plans but in thought and action.”

What does sustainability mean for you?

Luise Rosemeier: “To me, sustainability is like building a bridge that connects today’s world to the future. It’s not just about constructing a pathway that serves our immediate needs; it’s about ensuring that this bridge is strong, resilient, and inclusive.

The three main pillars of this bridge are the environment, society, and economy. The environmental pillar represents our commitment to the planet, ensuring that we don’t deplete resources or harm ecosystems. The societal pillar stands for fairness, equity, and community well-being, recognizing that every person’s welfare contributes to our collective success. The economic pillar emphasizes growth and progress but in a responsible, ethical manner.

Just as a bridge requires careful design, alignment, and maintenance, sustainability requires us to thoughtfully balance these three pillars. We must build our bridge in a way that not only serves us today but can support the journey of future generations. It’s about a thoughtful, intentional approach that respects our interconnectedness and responsibility to each other and to the world we share.”

What motivates you to work in sustainability?

LR: “Working in sustainability is more than a job for me; it’s a commitment to the future. Having a little son, I often find myself thinking about the world he’ll grow up in. What drives me every day is the desire to contribute to a planet that will not only sustain his generation but those to follow.

It’s not just about recycling or reducing emissions; it’s about a mindset shift that supports responsible growth and development. By being mindful of our choices, whether in business, politics, or daily life, we can create a world that thrives on balance and respect for nature.

In short, my motivation is rooted in love—for my family, for humanity, and for the Earth. I want to play my part in leaving behind a legacy that’s not only prosperous but also kind and responsible.”

What would you rate your most successful measure for more sustainability in the last years, and why?

LR: “Reflecting on our sustainability efforts at Wünsche Group, we’ve pursued a balanced and committed approach.

First, on the social compliance front, we’ve laid emphasis on human rights and fair working conditions in our supply chains. Our extensive Social Compliance Monitoring System reflects our strong commitment to transparency and accountability. Despite our own efforts, we are actively engaged in collaboration with industry initiatives like amfori and the Accord, both in Bangladesh as well as Pakistan, to enable continuous improvement for the well-being of the workers in our supply chains.

In the environmental domain, we have taken meaningful strides. The establishment of a process for the accounting of our Scope 3 emissions, though a complex process, has provided a more detailed insight into our CO2 footprint. This, along with the establishment of an environmental management system and our responsible chemical and wastewater management, lays the foundation upon which we build our environmental efforts. It’s the starting point for developing and implementing a strategy that includes ambitious targets and effective measures.”

How did you become a sustainability manager?

LR: “I began my career as a political scientist, consulting on large-scale projects in the energy and infrastructure sector in Africa. Yet, my passion for sustainability kept calling me. Realizing the pressing issue of climate change, I decided to pursue a master’s degree in International Business and Sustainability at the University of Hamburg. I have since gained hands-on sustainability experience across various industries like retail, food, textiles, hard goods, and electronics.

Currently, I work as a Corporate Responsibility Manager at Wünsche Group, where I actively contribute to driving sustainability initiatives within the company.

Becoming a sustainability professional was not just a career move but a culmination of lifelong learning, activism, and a profound desire to make a difference. It’s a role that allows me to combine my academic knowledge, professional skills, and personal passion to contribute positively to the world.”

What do you do to make your own life more sustainable?

LR: “Sustainability has been a core value for me, shaped by my upbringing in an eco-conscious household. A major turning point for me was learning about the plastic island floating in our oceans, which inspired me to become a Zero Waste activist for many years. Over time, I’ve recognized climate change and global warming as the most pressing issues. This realization has led me to adopt more climate-conscious practices in my daily life. I’ve shifted to a more plant-based lifestyle, focusing on responsible consumption and reducing waste. Traveling is an area where I’ve made a significant change; I have avoided flying for several years, opting for more sustainable modes of transportation. In line with this commitment to sustainability, my family has been living car-free forever, further reducing our environmental impact.

I’m also active politically as a member of the Green Party in Hamburg, working on local initiatives and policies that align with my values. While these actions might seem like small choices in the grand scheme of things, they’re part of my broader effort to live responsibly and encourage others to do the same. For me, sustainability isn’t about grand gestures; it’s about consistent, thoughtful choices that align with a more sustainable future.

What’s something new you learned in the past year?

LR: “In the last year, one profound realization I’ve come to embrace is the transformative power of adaptability. As the world around us rapidly evolves, it has become increasingly evident that the most resilient individuals and organizations are those that can adapt and pivot quickly. Instead of resisting change or clinging to outdated models, embracing uncertainty and cultivating a mindset of continuous learning is paramount. This lesson has reinforced the importance of flexibility, not just in strategies or plans but in thought and action. Whether facing global challenges like the pandemic or the intricate nuances of sustainability, adaptability is the cornerstone of progress and success.”

What do you think companies lack to become better at sustainability?

LR: “Sustainability is more than just a buzzword; it’s a fundamental shift in how businesses operate. What many companies seem to lack is holistic thinking. While many firms are embracing sustainability in some parts of their business, few see it as an integral part of every decision, from supply chain to consumer engagement. This segmented approach limits the potential impact and often leads to isolated initiatives that might be well-intentioned but fall short in creating systemic change.

Furthermore, the business world often gravitates towards quantifiable outcomes, understandably so. However, sustainability metrics can be challenging to define and measure. Instead of getting discouraged or focusing on short-term wins, companies need to prioritize long-term sustainable strategies, even if the benefits aren’t immediately quantifiable.

Lastly, the siloed nature of businesses today hinders collaboration. To genuinely drive sustainability, cross-functional cooperation and industry-wide collaborations are vital. Just as ecosystems thrive through biodiversity and interconnectivity, businesses need to cultivate diverse perspectives and partner beyond their usual scope. Only by doing so can we reimagine and rebuild systems that serve both our planet and its people.”

What do you think the world needs most to fight global warming and pollution?

LR: “The fight against global warming and pollution requires a collective realization that we are part of an interconnected ecosystem. First and foremost, this means shifting away from linear thinking and embracing a more systemic approach, where we recognize that our actions reverberate throughout the world. We need a shift from the ‘me-first’ mentality to a ‘we-first’ philosophy.

The challenge is immense, but I believe the solutions lie in collaboration, innovation, and a shared sense of responsibility. This includes governments creating incentives for clean energy, businesses prioritizing sustainability, and individuals making conscious choices in their consumption. Every stakeholder has a part to play, and no action is insignificant. What’s crucial is that we all start acting now.

We also need to foster an environment that encourages creative solutions. This includes investment in research and development, supporting startups with sustainable innovations, and creating platforms for dialogue across sectors and industries. If we truly want to make progress, we must be willing to explore new paradigms and be courageous enough to challenge our existing systems.”

What’s the biggest thing hindering you from implementing changes for more sustainability?

LR: “One of the substantial obstacles to implementing sustainable changes is the mindset that prioritizes immediate economic growth over long-term environmental responsibility. Too often, sustainability measures are seen as costly burdens rather than vital investments in our future.

This narrow focus on short-term costs can hinder progress, as it overlooks the broader benefits of sustainability and the potential risks of inaction. However, I believe that we’re gradually recognizing that the real costs lie in ignoring sustainability.”

If you had one wish from a legislative point of view to make your job easier – what would you wish for?

LR: “If I were to pinpoint one wish from a legislative perspective, it would be the establishment of a comprehensive, unambiguous, and universally adopted set of sustainability standards. Currently, companies navigate a labyrinth of fragmented guidelines and regulations, leading to inefficiencies and sometimes even conflicting efforts. A harmonized, globally recognized framework would streamline efforts, eliminate the guesswork, and ensure that everyone is working from the same playbook. Furthermore, this would hold organizations accountable, fostering a transparent and competitive environment that drives genuine sustainability advancements rather than mere box-ticking exercises. While achieving consensus on such a framework is undeniably challenging, the rewards in terms of clarity, efficiency, and collective progress would be immense.”

If you had one wish from your manager and your colleagues – what would you wish for?

LR: “My wish from both my managers and colleagues would be a continuous commitment to breaking down barriers and fostering collaboration across various functions and departments. Sustainability, innovation, and progress are not confined to single divisions but require a holistic approach where every individual contributes their expertise and perspective. I hope for an environment where we openly discuss challenges and fears, and where creativity and interdisciplinary exchange are encouraged. By embracing this collective approach, we can create solutions that are more robust, balanced, and capable of driving real transformation. Change doesn’t happen in isolation; it thrives when everyone participates, learns, and grows together.”

In response to the pressing need for sustainable and environmentally conscious practices, the Ecodesign for Sustainable Products Regulation (ESPR) has emerged as a significant milestone. Originating from the groundwork laid by the initial Ecodesign Directive of 2009, this regulation represents a vital step forward in shaping a greener future. The Ecodesign Directive set the stage by introducing energy-related standards and labels for a range of products, fostering energy efficiency and substantial savings for consumers. With the advent of the ESPR, the focus broadens, encompassing a wider array of goods and charting a path towards enhanced environmental sustainability through improving circularity, energy performance and other environmental sustainability aspects. As we navigate through the facets of the ESPR – from its overarching objectives to the innovative Digital Product Passport – we gain insight into its implications for industries, businesses, and consumers alike. This article embarks on a journey to explore the significance, implications, and timeline of the ESPR, shedding light on its role within the larger landscape of sustainable practices.

Why was the ESPR put into place?

The initial Ecodesign directive, established in 2009, set the foundation for today’s Ecodesign for Sustainable Products Regulation (ESPR). The Ecodesign Directive established energy-related criteria for specific products, conveyed through energy labels, and covered 31 product categories, predominantly energy-related items such as kitchen appliances. By 2021, these measures resulted in substantial benefits, saving EU consumers 120 billion in energy expenses and reducing annual energy consumption by 10% within the specified product range. The ESPR will not only expand the scope but also replace the former Ecodesign Directive. It stands as a key component of the Commission’s strategy for promoting environmentally sustainable and circular products, aligning closely with the Circular Economy Action Plan of March 2020, which in turn derives from the European Green Deal of 2019.

What is the ESPR?

The ESPR aims to expand the Ecodesign directive’s focus from energy-related products to encompass a broader range of goods. It outlines performance and information criteria for almost all types of physical items available in the EU market, though certain exceptions like food and feed apply. The proposal will add new requirements to the EU Ecodesign directive while also providing clarity on existing ones.

Central to this initiative is the establishment of a comprehensive framework to define ecodesign requirements tailored to specific product categories. The goal is to enhance the circularity, energy efficiency, and overall environmental sustainability of these products. A notable aspect of the ESPR is its emphasis on product information, with the introduction of concepts like the Digital Product Passport (DPP).

The initial focus for delegated acts under the ESPR is directed towards textiles and footwear in the realm of end-user products. Additionally, for intermediary products, the priority lies in iron and steel.

The Digital Product Passport

The Digital Product Passport, alongside Ecodesign criteria, will be introduced by the ESPR for all regulated products. This new passport will offer comprehensive information on the environmental sustainability of products to supply chain participants, regulators, and consumers. Accessible through data carrier scanning, it will encompass attributes like durability, reparability, recycled content, and spare part availability, aiming to empower consumers and businesses with informed purchasing decisions, streamline repairs and recycling, and enhance transparency regarding the environmental impact across a product’s lifecycle.

Which companies must comply with the ESPR?

The scope of ESPR compliance extends to all products introduced to the EU market, irrespective of their origin within or outside the EU. This proposal encompasses a wide range of products, extending beyond consumer goods, and even includes systems like military technology, space innovations, and medical apparatus. The addressed parties under the ESPR framework comprise economic entities throughout the value chain, encompassing product manufacturers, EU importers, distributors, retailers, sellers, and fulfillment service providers.

ESPR status and timeline

The current Ecodesign Directive continues to be operational until the transition to the ESPR. Currently, the European Union is in the process of drafting new regulations and conducting studies as part of the ESPR Work Plan, preceding the enforcement of the ESPR. Within the ESPR, each regulated product group has a distinct “implementing act.” The EU is actively developing and revising these acts for both new and existing product groups, with the new acts taking effect under the existing Ecodesign directive. Upon the ESPR’s implementation, it will supplant the current directive and take over these acts. The upcoming work plan for 2022-2024 entails implementing acts for mobile phones, tablets, computers, and computer servers. A total of 31 product categories are set for assessment, prioritizing those with the highest energy or material efficiency potential, potentially resulting in regulations by 2030. This phase emphasizes non-energy-related Ecodesign criteria such as durability, reparability, recyclability, end-of-life disassembly, reuse, and recycled content. The specifics of deadlines and transition periods are anticipated to be outlined in delegated acts post ESPR adoption, as its implementation is projected to span from 2024 to 2030.

How to prepare for the ESPR

Eco-design is only feasible when designers have data about the sustainability of their product, but also about its compliance, should costing, environmental, health, and safety criteria. A successful workaround in-between all teams can only be provided by integrating all the data needed. An LCA analysis of the product portfolio can ideally prepare companies for the ESPR and the DPP.

Conduct a Life Cycle Analysis of your portfolio

Implementing Life Cycle Assessment (LCA) within a product portfolio is an invaluable strategy for proactively aligning with the Ecodesign for Sustainable Products Regulation (ESPR). LCA, a comprehensive method that evaluates the environmental impacts of a product throughout its entire lifecycle, equips businesses with crucial insights into the environmental hotspots and opportunities for improvement within their product offerings. By conducting LCAs across the portfolio, companies can identify areas where resource consumption, emissions, and waste generation are most significant, allowing them to prioritize and optimize design, production, and end-of-life processes. This strategic approach not only ensures compliance with ESPR’s stringent sustainability requirements but also fosters innovation by promoting the development of more eco-friendly, energy-efficient, and resource-conscious products. Moreover, by quantifying and disclosing the environmental performance of their products, businesses can be prepared for the Digital Product Passport and enhance consumer trust.

Conclusion

In response to the imperative for sustainable practices, the emergence of the Ecodesign for Sustainable Products Regulation (ESPR) marks a significant milestone. Building upon the foundation set by the Ecodesign Directive of 2009, this regulation represents a noteworthy progression towards ecological awareness. The initial directive introduced energy-related standards and labels, fostering efficiency and savings. With the ESPR, the scope broadens to encompass a wider range of goods, expanding the focus on environmental sustainability. As businesses and industries adapt to comply with the ESPR, they engage in a journey towards a future where responsible product design harmonizes with ecological stewardship.

Sustainability reporting has gained significant importance over the years as companies and investors recognize the value of understanding a business’s impact on the environment and society. In 2014, the European Union (EU) introduced the Non-Financial Reporting Directive (NFRD) to encourage companies to disclose non-financial information related to environmental, social, and governance (ESG) matters. However, with the aim of strengthening sustainability reporting and ensuring it carries the same weight as financial reporting, the EU has decided to replace the NFRD with the Corporate Sustainability Reporting Directive (CSRD). In this article, we will explore the key aspects of the CSRD and how companies can prepare for compliance with this new directive.

Why was the CSRD put into place?