Published 14.01.23

The EU Carbon Border Adjustment Mechanism (CBAM)

In a bid to combat carbon emissions and level the playing field for European businesses, the European Union (EU) has introduced the Carbon Border Adjustment Mechanism (CBAM).

In a bid to combat carbon emissions and level the playing field for European businesses, the European Union (EU) has introduced the Carbon Border Adjustment Mechanism (CBAM). This mechanism, part of the EU’s “Fit for 55” package, aims to put a price on greenhouse gas emissions associated with imports compared to products produced within the EU. It also ensures that domestic manufacturers have equal competitive opportunities concerning greenhouse gas costs compared to their counterparts in non-EU countries.

Why was CBAM implemented?

The EU’s goal is ambitious: to reduce carbon dioxide (CO2) emissions by 55% by 2030 compared to 1990 levels. As part of this initiative, the EU has been gradually reducing the free allocation of EU Emissions Trading System (EU-ETS) certificates to energy-intensive industries. This reduction creates a risk of companies in certain sectors shifting their production to Non-EU countries due to cost considerations, potentially undermining the effectiveness of the EU’s emissions reduction measures.

While EU-based businesses are already required to account for the carbon footprint of their production, CBAM extends this requirement to businesses importing goods from outside the EU, making importers of CBAM-covered products pay a carbon price to mitigate potential competitive disadvantages for domestic manufacturers of similar goods.

What is CBAM?

CBAM necessitates a carbon price on the import of specific goods produced outside the EU based on their associated carbon emissions. The price per CBAM certificate is determined by the average weekly price of EU Emissions Trading System (EU-ETS) certificates and multiplied by the number of CBAM certificates to be surrendered. Each CBAM certificate corresponds to one tonne of emitted CO2 (carbon dioxide), N2O (nitrous oxide), or F-gases (perfluorinated hydrocarbons) released during the production process of the imported goods.

Importers can claim a reduction in the number of CBAM certificates to be surrendered if they can demonstrate that a carbon price was paid in the country of origin.

Which companies are affected by CBAM?

The following product categories are set to be included in CBAM starting from October 2023:

- Fertilizers (including precursor products such as ammonia and potassium nitrate)

- Cement (including bricks, clay cement, and other kaolin-containing clay and earthware)

- Iron (agglomerated iron ores and concentrates) and steel (including downstream products)

- Aluminum (including downstream products)

- Electrical energy

- Hydrogen

Important: CBAM applies for companies that import the above materials but also for companies that import processed goods containing the above materials (especially for aluminum and steel)

In the coming years, there are plans to expand the scope of CBAM to include all goods covered by the EU Emissions Trading System (ETS). Non-EU countries integrated into the EU Emissions Trading System or whose emissions trading systems are recognized as equivalent may be exempted from CBAM.

CBAM Status and Timeline

CBAM will be introduced gradually, beginning with a transitional phase from October 1, 2023, to December 31, 2025. During this period, companies will be required to calculate and document the direct and indirect emissions associated with the production process of imported goods subject to CBAM. They must submit quarterly reports, known as CBAM reports, by January 31, 2024, providing data on the quantity of imports, direct and indirect CO2 emissions abroad, and the potential carbon price paid in the country of origin. The CBAM report is submitted using the CBAM Transitional Registry which will be deployed for the use of Economic Operators in the EU as from the 1st of October 2023 together with a set of webinars and trainings which will facilitate the use of the registry and the submission of data during the transitional period. However, no financial compensation through the surrender of CBAM certificates is required during this phase.

Find more information here.

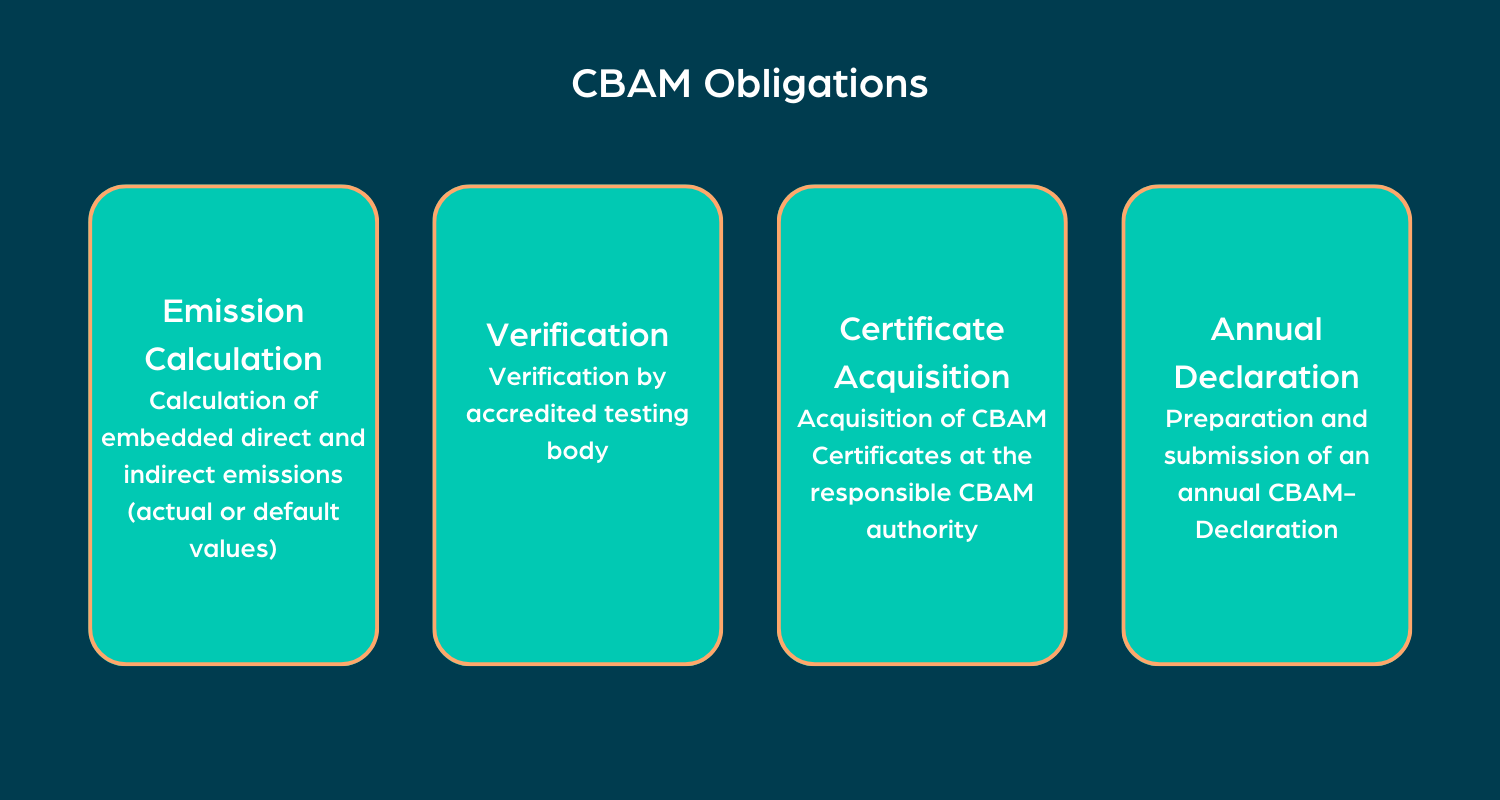

From January 1, 2026, CBAM will fully come into effect. At this point, companies will face more extensive obligations, including the need for a CBAM registration for the status of an “Authorized Declarant.” They must calculate the embedded direct and indirect emissions of imported goods into the EU, have the reported data on direct and indirect emissions verified by an accredited testing body, purchase the required number of CBAM certificates through a central platform to cover the embedded direct and indirect emissions, and submit an annual CBAM declaration by May 31 of each calendar year for emissions associated with goods imported in the previous year.

![]()

How to prepare for CBAM

Preparing for the implementation of the Carbon Border Adjustment Mechanism (CBAM) requires proactive measures. Companies should begin by conducting a comprehensive assessment of their supply chains to identify products that fall under CBAM’s purview. This involves calculating the direct and indirect emissions associated with their imported goods and considering potential carbon pricing mechanisms in the countries of origin. To streamline compliance, businesses should invest in robust data collection and reporting systems. Additionally, they should monitor updates and guidelines provided by regulatory authorities to ensure alignment with CBAM requirements. Ultimately, preparation for CBAM hinges on a combination of thorough assessment, technological readiness, and collaboration between public and private sectors to navigate the transition successfully.