Published 29.02.24

Guideline: The European Green Deal and Sustainability Regulation emerging from it

As the world faces increasing environmental challenges, the EU’s approach to sustainability regulation sets a precedent for other regions to follow and collectively work towards a more sustainable and resilient future.

The European Union (EU) stands out as a global leader in enacting highly sophisticated, stringent, forward-thinking, and intricate corporate and investor sustainability laws, along with comprehensive reporting requirements within its economic domain. Embracing the overarching ‘European Green New Deal’, Europe is actively executing an extensive array of measures aimed at combatting climate change, fostering sustainable innovation, and achieving climate neutrality across the continent by 2050. In this guide, we will delve into the European Green Deal, examining its core elements and the reporting regulations it entails, while assessing whether the regulations and directives represent solely an additional task or a unique opportunity.

The European Green Deal

The European Green Deal is a comprehensive and ambitious policy framework introduced by the European Commission, the executive branch of the European Union, in December 2019. It serves as a roadmap and action plan to transform the EU into a sustainable, climate-neutral, and environmentally friendly economy by 2050. The deal aims to tackle climate change, biodiversity loss, and environmental degradation while promoting a just and inclusive transition.

Why was the European Green Deal put into place?

The roots of the European Green Deal can be attributed to several key factors. Firstly, the adoption of the Paris Agreement in 2015 laid the foundation for international efforts to limit global warming to below 2 degrees Celsius, with an ambitious target of 1.5 degrees Celsius. As a party to the agreement, the EU made commitments to take bold measures in reducing greenhouse gas emissions.

Additionally, there has been a noticeable shift in politics, with EU member states, policymakers, and citizens recognizing the urgency of addressing climate change and embracing environmental protection and sustainability as fundamental priorities for the region.

Moreover, the rise of environmental movements and increased public awareness and activism has exerted significant pressure on political leaders, compelling them to take more decisive actions towards achieving sustainability goals. These factors combined have paved the way for the formulation and implementation of the European Green Deal, signaling the EU’s commitment to leading the fight against climate change and promoting a greener and more sustainable future.

How does the European Green Deal work?

The European Green Deal acts as a guiding roadmap and action plan, directing the EU’s policies and initiatives for the foreseeable future. Its implementation involves a multifaceted approach, comprising legislative measures, funding mechanisms, and collaborative efforts with member states, businesses, civil society, and international partners.

Under the umbrella of legislation and regulation, the European Commission formulates and enacts new laws and regulations to support the Green Deal’s objectives. This entails establishing targets, standards, and guidelines aimed at promoting sustainable practices across various sectors.

To facilitate the realization of its goals, the EU provides substantial funding through diverse mechanisms such as the Just Transition Fund, the European Green Deal Investment Plan, and the EU’s long-term budget (Multiannual Financial Framework).

The success of the Green Deal hinges on fostering cooperation and partnerships with EU member states, businesses, local authorities, and civil society organizations. This collaborative approach is crucial for effective implementation and continuous monitoring of the initiatives.

Regular monitoring and reporting by the EU play a vital role in evaluating the progress made towards achieving the Green Deal’s objectives. This fosters transparency, ensures accountability, and allows for necessary policy adjustments and actions as circumstances evolve.

The European Green Deal Objectives

The European Green Deal represents a collective effort by the EU to address the pressing challenges posed by climate change and environmental degradation while fostering economic growth and social well-being within a sustainable framework. It involves legislation, funding mechanisms, and collaborations between member states, industries, and civil society to achieve its ambitious goals. Key objectives of the European Green Deal include:

- Climate Neutrality: The primary goal is to make Europe the world’s first climate-neutral continent by 2050. This entails reducing greenhouse gas emissions to net-zero levels, where any remaining emissions are offset by measures such as carbon capture or reforestation.

- Clean Energy: The deal emphasizes the adoption of renewable and clean energy sources, reducing reliance on fossil fuels, and promoting energy efficiency to achieve a sustainable energy system.

- Circular Economy: The EU aims to transition towards a circular economy that minimizes waste, promotes recycling, and encourages the sustainable use of resources.

- Biodiversity and Ecosystems: The Green Deal aims to protect and restore biodiversity, enhance ecosystem resilience, and combat pollution to ensure the long-term health of the environment.

- Sustainable Agriculture and Food Systems: The deal seeks to promote sustainable agricultural practices, reduce the environmental impact of food production, and support more sustainable food consumption patterns.

- Sustainable Mobility: The EU aims to promote clean and sustainable transport options, including increased use of electric vehicles, improved public transportation, and cycling infrastructure.

- Renovation of Buildings: The Green Deal emphasizes improving the energy efficiency of buildings to reduce emissions and enhance the overall sustainability of the construction sector.

- Just Transition: The deal emphasizes the importance of a fair and inclusive transition, ensuring that the changes in economic and industrial practices do not disproportionately affect vulnerable communities and workers.

Source: EUinASEAN

An Overview: European Sustainability Reporting Regulations

The European Green Deal entails various reporting regulations aimed at monitoring and assessing progress towards its sustainability goals. These reporting regulations aim to enhance transparency, accountability, and informed decision-making in pursuit of the European Green Deal’s ambitious sustainability goals. By requiring organizations to disclose their environmental and climate-related data, the EU seeks to drive positive change and ensure a collective effort towards building a climate-neutral and environmentally responsible continent.

Circular Economy and Waste Management:

The EU has been actively promoting a circular economy model, which aims to minimize waste, extend product lifetimes, and enhance resource efficiency. This section explores EU directives and regulations concerning waste management, recycling, and eco-design, as well as the promotion of sustainable production and consumption patterns.

Ecodesign for Sustainable Products Regulation (ESPR)

What is it?

The ESPR aims to expand the Ecodesign directive’s scope to cover a wide range of goods beyond energy-related products. It sets criteria for most physical items in the EU market, excluding some like food. It enhances eco-friendliness and energy efficiency through tailored ecodesign requirements. Notably, it introduces the Digital Product Passport (DPP) for better product information.

Who needs to comply?

All companies introducing products to the EU market, regardless of origin, must comply with the ESPR. This includes a wide range of products, even extending to military, space, and medical items. The ESPR framework covers various entities in the value chain, such as manufacturers, importers, distributors, retailers, and sellers.

When does it come into action?

The current Ecodesign Directive is active until the transition to the ESPR. The ESPR will replace the current directive upon implementation. The 2022-2024 work plan includes acts for mobile phones, tablets, computers, and servers. 31 product categories will be assessed, focusing on energy and material efficiency, potentially leading to regulations by 2030. The phase emphasizes criteria like durability, reparability, and recyclability. Deadlines and transitions will be detailed in post-ESPR adoption delegated acts, as implementation is expected from 2024 to 2030.

Find detailed info about the ESPR here.

Digital Product Passport (DPP)

The Digital Product Passport (DPP) is a concept introduced under the Ecodesign for Sustainable Products Regulation (ESPR). It aims to provide comprehensive and standardized information about a product’s environmental and sustainability attributes throughout its entire lifecycle. The DPP is a digital document or database that accompanies a product from its design and manufacturing stages to its use, maintenance, and eventual disposal or recycling.

Key features of the Digital Product Passport:

- Product Information: materials, components, energy efficiency, environmental impact, repairability, etc.

- Lifecycle Data

- Repair and Maintenance: guidelines for repairing and maintaining the product, extending its lifespan and reducing the need for premature disposal

- Recycling and Disposal: how the product can be disassembled, recycled, or disposed of properly

- Traceability and Transparency: a traceable record of the product’s origin, manufacturing processes, and environmental impact

The introduction of the Digital Product Passport is aimed at fostering a more sustainable approach to product design, manufacturing, and consumption. It empowers consumers to make environmentally conscious choices, encourages manufacturers to produce longer-lasting and more eco-friendly products, and contributes to the overall transition towards a circular economy.

Sustainable Finance and Investment:

The EU is working on aligning financial systems with sustainability objectives. This section covers the EU Taxonomy for sustainable activities, the Sustainable Finance Disclosure Regulation, and other measures to encourage green investments and responsible financial practices.

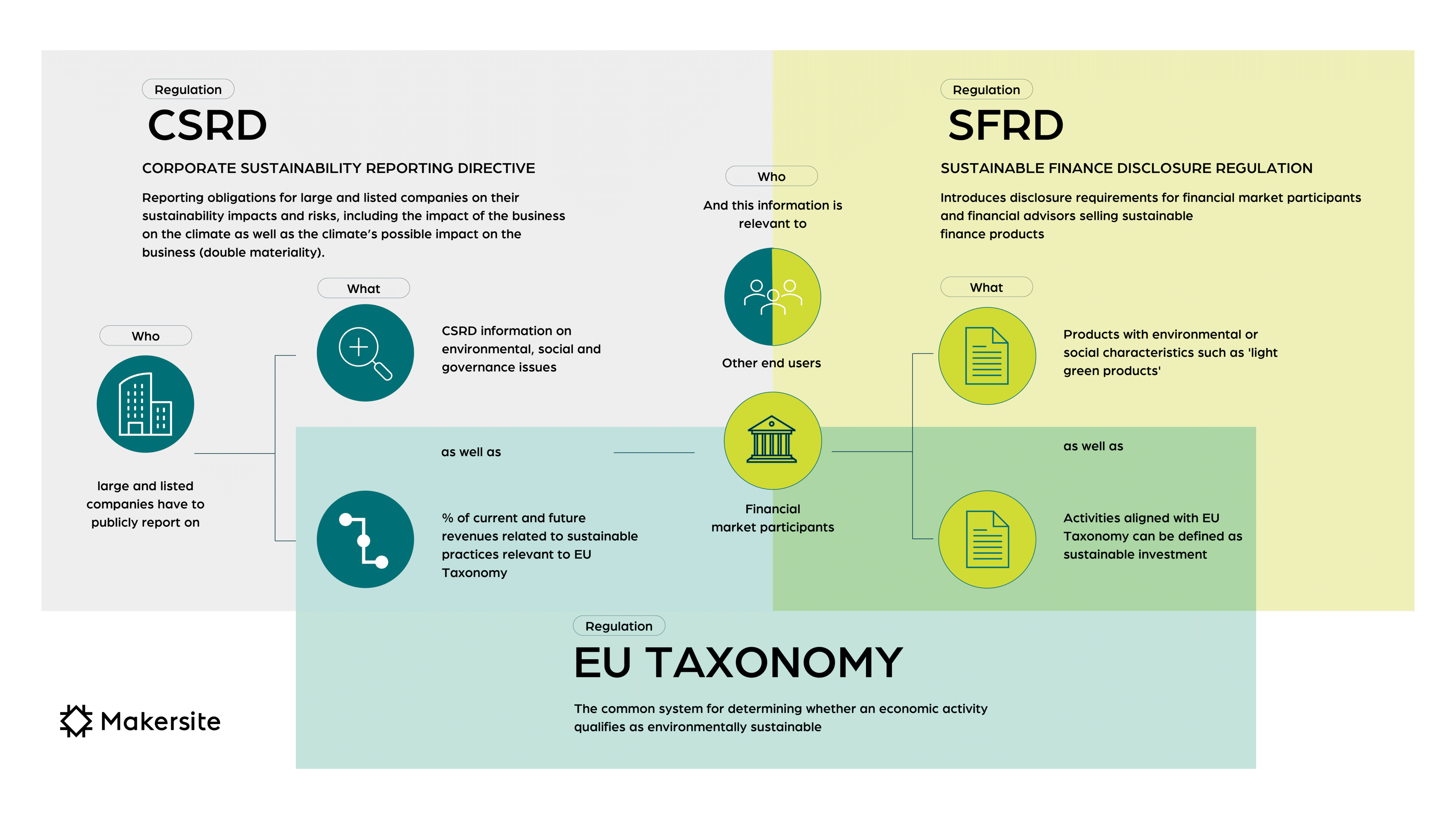

Sustainable Finance Disclosure Regulation (SFDR)

What is it?

The Sustainable Finance Disclosure Regulation (SFDR) is a financial reporting framework that promotes transparency regarding sustainability. It mandates financial market participants and advisors to reveal how they address sustainability risks and impacts in their products. Suppliers of investment products must disclose how they communicate sustainability considerations to clients. SFDR aims to enhance transparency in the sustainability of financial offerings and prevent misleading claims of sustainability (greenwashing) often associated with investment funds.

Who needs to comply?

SFDR compliance is necessary for financial market participants (FMPs) and financial advisors. Any company involved in creating and offering financial products must adhere to SFDR, alongside existing disclosure requirements.

When does it come into action?

The SFDR has been in place since 2019 and the concerned parties need to report against it since 2021.

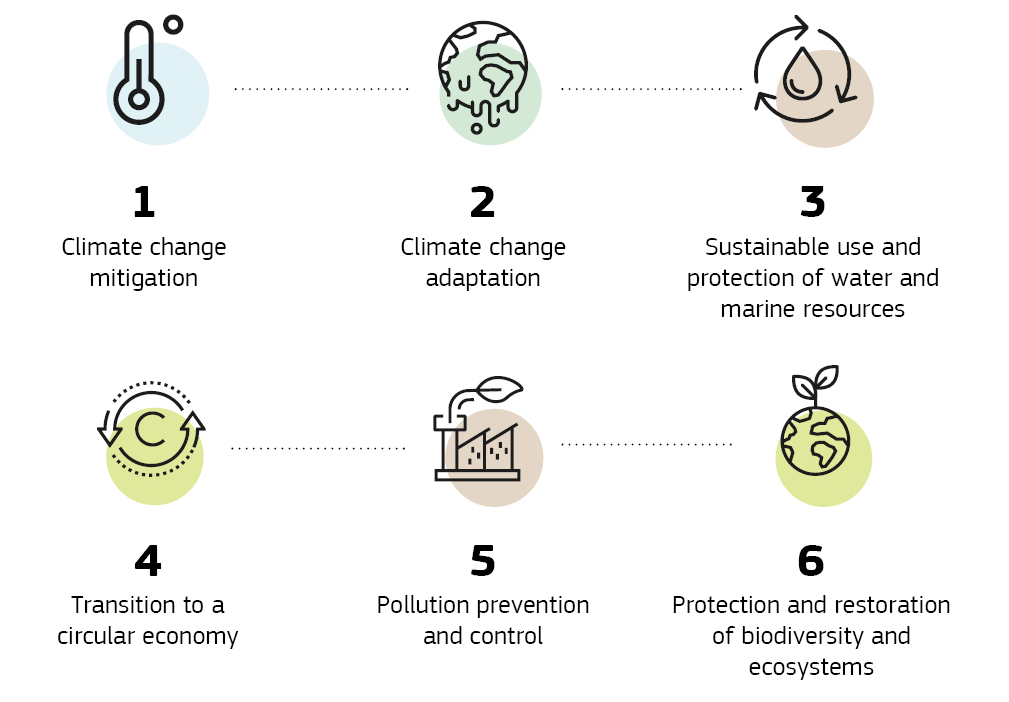

EU taxonomy

What is it?

The EU Taxonomy is a guide that categorizes economic activities as environmentally sustainable or not. Starting in 2023, companies and investors must report how well their actions align with it. This helps measure their level of environmental friendliness. The Taxonomy focuses on six goals, including climate action, water protection, and circular economy. Financial institutions will report on the first two goals from January 1, 2023, with the remaining four added a year later.

Source: European Commission

Who needs to comply?

The reporting obligation extends to all financial market participants, large companies, and SMEs listed on the stock exchange. If a company is based in Europe or operates a European legal entity with more than 500 employees, reporting is mandated.

When does it come into action?

The EU Taxonomy will be implemented in stages. Starting from January 1, 2023, financial institutions will need to report the portion of their portfolio aligned with the EU Taxonomy. Initially, they will report on two environmental objectives related to climate change. The other four objectives will be added a year later. This reporting requirement applies to EU-registered companies for now.

Find detailed info about EU taxonomy here.

Task Force on Climate-related Financial Disclosures (TCFD)

The Task Force on Climate-related Financial Disclosures (TCFD) is a reporting standard designed to encourage organizations to disclose information about their climate-related financial risks and opportunities. It was established by the Financial Stability Board (FSB) in 2015 and provides a framework for companies to voluntarily disclose information related to their governance, strategy, risk management, and metrics in relation to climate change. The TCFD framework aims to enhance transparency, enable better assessment of climate-related risks, and help investors, lenders, and other stakeholders make more informed decisions regarding the financial implications of climate change on businesses.

Corporate Social Responsibility and Reporting:

The EU has taken steps to encourage corporate social responsibility and sustainability reporting by businesses. This part discusses the Corporate Sustainability Reporting Directive (CSRD) and other initiatives that promote transparency and accountability in corporate sustainability practices.

The Corporate Sustainability Reporting Directive (CSRD)

What is it?

The CSRD, or Corporate Sustainability Reporting Directive, builds upon the NFRD by expanding reporting requirements for companies on ESG matters like environmental impact, social policies, and human rights. It introduces new aspects such as reporting future-oriented sustainability goals, adverse effects, and intangible resources. The CSRD also introduces “double materiality,” compelling companies to consider both their impact on the environment and potential environmental impacts on their future, while mandating independent verification, integration of sustainability reporting into management reports, and the use of machine-readable formats for transparency. The European Financial Reporting Advisory Group (EFRAG) is developing reporting standards to ensure consistency and transparency.

Who needs to comply?

The CSRD requires compliance from NFRD-reporting companies and includes new criteria: firms with 250+ employees, €40M+ net sales, or €20M+ balance sheet, plus most listed companies (except small ones) and non-EU companies with €150M+ EU sales for two years.

When does it come into action?

The NFRD rules are effective until CSRD implementation. Starting January 2024, large public interest companies (500+ employees) must follow CSRD. From January 2025, other eligible companies must comply. By January 2026, stock-exchange-listed SMEs (without postponement) also need to adhere to CSRD.

However, in October 2023 the European Commission announced plans to delay key aspects of CSRD, specifically the adoption of requirements for companies to provide sector-specific sustainability disclosures and for sustainability reporting from companies outside of the EU.

Announced alongside the Commission’s release of its 2024 Commission Work Programme – designed to set out a list of actions it will take over the upcoming year – the statement outlines the EU Commission’s intention to postpone the adoption date for the sector-specific European Sustainability Reporting Standards (ESRS) by two years. Additionally, it recommended delaying the adoption of rules for large non-EU companies that operate in the EU to provide sustainability reporting by 2 years.

As the Commission notes in its proposal, the postponement of these two key rules has arisen in order to allow “companies to focus on the implementation of the first set of ESRS,” “ensure that EFRAG has time to develop sectoral ESRS that are efficient,” and “limit the reporting requirements to the minimum necessary.”

Find detailed info about the CSRD here.

Corporate Sustainability Due Diligence Directive (CSDDD)

What is it?

Note: Further CSDDD developments – where the directive failed to receive final approval – were announced on 28th February 2024. You can read about what happened here.

The CSDDD is an EU directive inspired by French and German laws, aiming to make companies address environmental and human rights risks in supply chains. It mandates risk assessment and mitigation, requiring large firms to align strategies with a sustainable economy and 1.5°C global warming limit. Proposed penalties of up to 5% of global sales are included for violations.

Who needs to comply?

The proposed directive lowers the threshold for companies affected, now including those with 250+ employees and over 40 million euros global turnover (compared to the earlier draft’s 500 employees and 150 million euros). Transition periods of up to five years are proposed to accommodate varying company sizes.

When does it come into action?

In 2023, the CSDDD has advanced significantly, with MEPs voting to enhance the original proposal. It’s currently in trilogue stage for negotiation among the European Parliament, Commission, and Council. A decision is expected soon, leading to implementation and mandatory company compliance with the directive’s provisions.

Find detailed info about the CSDDD here and information about what the implementation of the CSDDD could mean to your role here.

Green Claims Directive

What is it?

The Green Claims Directive enhances consumer protection rules, applying to both B2C and B2B marketing for explicit environmental claims. It mandates substantiation with scientific evidence, comprehensive life-cycle assessment, transparency in offsets, and a holistic approach to evaluating environmental impact. The directive complements existing regulations and emphasizes robust verification of environmental claims.

Who needs to comply?

The Green Claims Directive will impact most EU companies, including SMEs and large corporations in diverse sectors, and also non-EU companies targeting EU consumers. However, very small micro-SMEs (under ten employees or less than €2 million annual turnover) will be exempt from the requirements.

When does it come into action?

The European Commission introduced the Green Claims Directive on March 22, 2023. After its enactment, Member States will have 18 months to adopt it into their national laws. While implementation is anticipated by 2026, the timeline could shift based on EU negotiations.

Find detailed info about the Green Claims Directive here.

European Sustainability Reporting Standards (ESRS)

In order to guarantee uniformity and openness in reporting, the European Financial Reporting Advisory Group (EFRAG) is in the process of formulating reporting standards for the CSRD, the so called European Sustainability Reporting Standards. The initial segment of these standards was projected to be released by November 2023, with the subsequent segment scheduled for publication in June 2024, but an October 2023 announcement by the EU Commission (see ‘The Corporate Sustainability Reporting Directive’, above) outlined their intention to postpone the adoption date for ESRS by 2 years.

Excerpt: Why Global Companies need to care about European Regulation

Global companies need to care about European sustainability reporting regulations because it directly impacts their access to European markets and smooth operations within the EU. Many global companies conduct business in the European Union or trade with EU member states. Compliance with European sustainability reporting regulations is essential to access these markets and ensure smooth operations without facing potential trade barriers or legal penalties. Moreover, adhering to these regulations provides a competitive advantage in a market where sustainability is increasingly valued.

The global trend towards sustainability reporting indicates that similar regulations may emerge in other regions, making compliance with European standards a strategic move for long-term viability and adaptability. For companies with complex supply chains extending to the EU, aligning with these regulations is essential to ensure seamless operations and avoid disruptions.

Sustainability Reporting: Struggle or Chance?

Sustainability reporting stands as a crucial tool in our modern world, aiming to bring transparency and accountability to the environmental, social, and governance (ESG) aspects of organizations. Yet, this endeavor does not come without its challenges, as it navigates the ever-shifting landscape of business, regulation, and public perception.

One of the primary struggles that sustainability reporting faces is the tension between its intent and the potential for “greenwashing.” Greenwashing occurs when companies present themselves as more sustainable than they truly are, often by manipulating data or focusing on a few positive aspects while downplaying their negative impacts. This dilutes the credibility of sustainability reports and erodes the trust of stakeholders who are seeking genuine efforts toward a more sustainable future.

Furthermore, the lack of standardized frameworks and guidelines for sustainability reporting poses a significant hurdle. With various reporting standards, such as GRI, SASB, and integrated reporting, organizations must choose which approach to follow. This diversity not only makes it challenging to compare different companies’ performance but also creates confusion among stakeholders about the true environmental and social implications of a company’s operations.

Financial constraints also hinder the comprehensive adoption of sustainability reporting. Small and medium-sized enterprises (SMEs) often struggle to allocate resources for data collection, analysis, and reporting on sustainability efforts. The upfront costs of setting up robust tracking systems and hiring specialized personnel can be daunting, making it difficult for smaller players to participate fully in this movement.

Legal and regulatory inconsistencies across different jurisdictions further complicate the sustainability reporting landscape. With varying requirements and expectations, multinational companies must navigate a complex maze of rules, sometimes leading to discrepancies in how they report their sustainability progress. This can create skepticism about the accuracy and reliability of the information presented in these reports.

To overcome these challenges, collaboration is key. Governments, regulatory bodies, businesses, and civil society must work together to establish clear and consistent reporting standards that are applicable globally. Moreover, technological advancements can play a crucial role in streamlining data collection and analysis, reducing the resource burden on organizations, especially SMEs.

However, despite these challenges, the importance of sustainability reporting cannot be underestimated. As stakeholders, including investors, consumers, employees, and regulators, demand greater transparency and responsible business practices, the pressure on organizations to improve their ESG performance intensifies. Companies that embrace sustainability reporting genuinely and integrate it into their core strategies can gain a competitive advantage by building trust and goodwill with stakeholders.

Summary

The EU’s sustainability regulations are comprehensive and wide-ranging, covering numerous sectors and aspects of modern life. By examining and adhering to these guidelines, businesses, governments, and individuals can actively contribute to a greener and more sustainable future for Europe and the planet at large. As the world faces increasing environmental challenges, the EU’s approach to sustainability regulation sets a precedent for other regions to follow and collectively work towards a more sustainable and resilient future.